So, you've got a business and you want to keep track of where your money is going and how much you're making. That's where a Profit and Loss Statement (or P&L statement) comes in. It's essentially a financial report card that tells you if your business is in the green or the red. If you've ever wondered how to whip one of these up, you're in the right place. We'll break it down into bite-sized steps that make it feel less like a chore and more like a rewarding exercise.

Why You Need a Profit and Loss Statement

Before we get into the nitty-gritty of how to create a P&L statement, let's talk about why it's so important. Think of it as your financial GPS. Guiding you to make informed decisions. Want to know if that new marketing campaign is paying off? Check your P&L. Considering expanding your product line? Your P&L can help you figure out if you've got the funds to do so.

The P&L statement summarizes the revenues, costs, and expenses incurred during a specific period, usually a fiscal quarter or year. It's a snapshot of your business's ability to generate profit by increasing revenue, reducing costs, or both. It's not just for your eyes, though. Investors, lenders, and other stakeholders often look at P&L statements to gauge the health of a business.

Gathering the Necessary Information

Alright, let's get started. First, you'll need to gather some essential information. This is like gathering ingredients before you start cooking. Here's what you'll need:

- Revenue Data: This includes all the money your business has earned from selling goods or services. Make sure to include all revenue streams.

- Cost of Goods Sold: These are the direct costs attributable to the production of the goods sold by a company. This might include the cost of materials and labor directly used to create a product.

- Operating Expenses: These are the expenses required to run your business that aren't directly linked to producing goods or services. Think rent, utilities, and salaries.

- Other Expenses: This category can include interest, taxes, and other non-operating costs.

Having all this information at your fingertips will make the process smoother. A spreadsheet is a great place to start organizing this data. If you're looking for something more robust, Spell can help streamline the process by automatically generating and organizing your financial data.

Structuring Your Profit and Loss Statement

Once you've gathered your information, it's time to structure your P&L statement. Think of this as setting up the skeleton, which you'll fill in with all the juicy details later. Here's a basic outline you can follow:

Revenue:

- Sales Revenue

- Other Revenue

Cost of Goods Sold:

- Direct Materials

- Direct Labor

- Other COGS

Gross Profit: (Revenue - COGS)

Operating Expenses:

- Rent

- Utilities

- Salaries

- Marketing

- Depreciation

- Other Operating Expenses

Operating Income: (Gross Profit - Operating Expenses)

Other Income and Expenses:

- Interest Expense

- Taxes

- Other Income/Expenses

Net Income: (Operating Income - Other Expenses + Other Income)

This basic structure will guide you in organizing your numbers and telling a clear financial story. Remember, the goal is to make your P&L statement easy to read and understand, not just for you, but for anyone else who might need to look at it.

Calculating Revenue

Revenue is the total income generated by your business from its normal business operations. It can be tempting to just look at the top-line sales numbers. But don't forget about any other income streams. Maybe you have some investment income or rental income. Include those too!

To calculate revenue, add up all the sales from your primary business activities. If you offer multiple products or services, list each one separately and then total them. This transparency not only helps you but also provides clarity for others reviewing your statement.

For example, suppose your business sells coffee and pastries. Your revenue section might look like this:

Revenue:

- Coffee Sales: $50,000

- Pastry Sales: $30,000

- Total Revenue: $80,000

Keep it simple and straightforward. Revenue is all about what money comes in through the front door.

Determining Cost of Goods Sold

Next up, we have COGS, which stands for Cost of Goods Sold. This is essentially what it costs you to produce the goods or services you sell. It's a crucial component because it directly impacts your gross profit and overall profitability.

To calculate COGS, you'll need to sum up all the direct costs associated with producing your products. This can include:

- The cost of raw materials

- Direct labor costs

- Overhead costs directly tied to production

Here's how it might look for a bakery:

Cost of Goods Sold:

- Flour and Ingredients: $10,000

- Labor: $15,000

- Packaging: $2,000

- Total COGS: $27,000

Understanding COGS is key to pricing your products effectively. If this section feels overwhelming, remember that tools like Spell can help you automate these calculations, saving you time and reducing errors.

Calculating Gross Profit

Now that you've got your revenue and COGS down, it's time to calculate Gross Profit. This figure tells you how much money you're making after covering the costs of producing your goods. It's a crucial number because it indicates whether your core business operations are profitable.

The formula is simple:

Gross Profit = Total Revenue - Total COGS

Using our bakery example:

Gross Profit = $80,000 (Revenue) - $27,000 = $53,000

This number gives you a clear picture of how much money is left over to cover operating expenses, taxes, and other costs. If your gross profit is low, it might be time to revisit your pricing strategy or find ways to reduce production costs.

Listing Operating Expenses

Operating expenses are the costs necessary to keep your business running day-to-day. These include everything from rent and utilities to marketing expenses and salaries. Unlike COGS, operating expenses aren't directly tied to the production of goods or services.

Here's a list of common operating expenses to consider:

- Rent or lease payments

- Utilities (electricity, water, internet)

- Salaries and wages for administrative staff

- Office supplies

- Marketing and advertising

- Insurance

- Depreciation of assets

Let's say your bakery has the following operating expenses:

Operating Expenses:

- Rent: $12,000

- Utilities: $3,000

- Salaries: $18,000

- Marketing: $5,000

- Depreciation: $2,000

- Total Operating Expenses: $40,000

Listing these expenses gives you a clear understanding of where your money is going and helps identify areas to cut costs if needed.

Calculating Operating Income

Operating income, also known as operating profit, shows how much money your business makes from its core operations, excluding any income from investments or taxes. It's a solid indicator of how well your business manages its costs and generates profit.

To calculate operating income, use the following formula:

Operating Income = Gross Profit - Total Operating Expenses

For our bakery example:

Operating Income = $53,000 (Gross Profit) - $40,000 (Operating Expenses) = $13,000

This figure tells you how much profit is left after covering all operating expenses. If this number is low or negative, it might be time to reevaluate your business strategy to boost profitability.

Other Income and Expenses

Now, let's talk about other income and expenses. These are the financial activities that don't fit neatly into your business's core operations. They can include interest income, interest expenses, gains or losses from investments, and any unusual or one-time expenses.

Here's how you can structure this section:

Other Income and Expenses:

- Interest Expense: $1,000

- Taxes: $2,000

- Other Income: $500

- Total Other Expenses: $2,500

This section might seem like small potatoes. But these numbers can have a big impact on your net income. Keep a close eye on them to ensure they don't sneak up and surprise you.

Calculating Net Income

We've made it to the grand finale: calculating Net Income. This is the bottom line. The ultimate figure that tells you the profitability of your business after all revenues and expenses are accounted for.

Here's the formula:

[Net Income](/resources/how-to-write-an-income-statement) = Operating Income - Total Other Expenses + Other Income

Using our bakery example, the calculation would be:

Net Income = $13,000 (Operating Income) - $2,500 (Total Other Expenses) + $500 (Other Income) = $11,000

Congratulations, you've created a Profit and Loss Statement! This final number is what you, your investors, and your lenders will be most interested in. It's a clear indicator of your company's overall financial health.

Using Tools to Simplify the Process

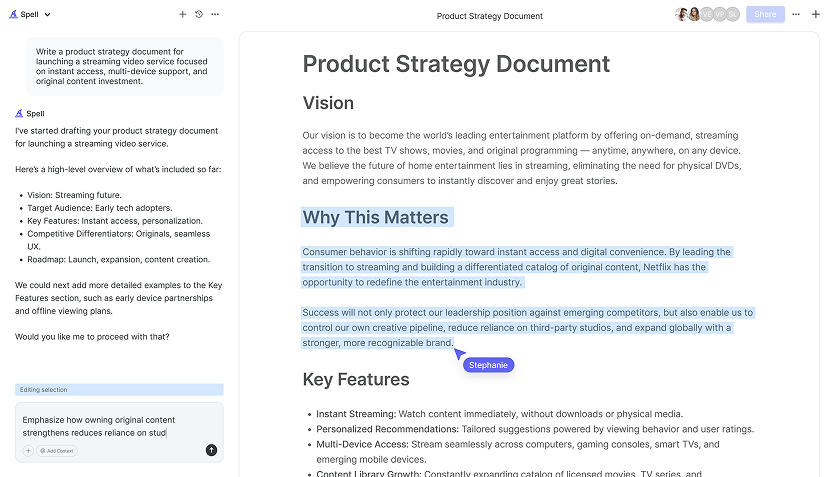

If all these calculations have your head spinning, don't worry. There are plenty of tools out there designed to make creating a P&L statement easier. One such tool is Spell. We offer an AI document editor that can help you draft and refine your P&L, saving you time and reducing errors.

With Spell, you can:

- Generate a polished draft of your P&L statement in seconds

- Edit and refine your document using natural language prompts

- Collaborate with your team in real-time

It's like having a financial advisor at your fingertips, helping you make sense of your numbers without the headache.

Final Thoughts

Writing a Profit and Loss Statement might seem intimidating at first. But once you break it down into manageable steps, it becomes a powerful tool for understanding your business's financial health. By tracking revenue, costs, and expenses, you gain valuable insights that can guide your business decisions. And with Spell, we make the process even easier, helping you create high-quality documents in a fraction of the time. Happy number crunching