Creating a financial statement might seem daunting at first, but it's a vital skill that can help you understand the financial health of a business or organization. Whether you're gearing up for a job in finance or just want to get a handle on your personal finances, knowing how to put together a financial statement is incredibly useful. This guide will walk you through the process. Breaking it down into manageable steps with clear examples along the way.

Why Financial Statements Matter

Financial statements are like the scorecards of a business. They give you a snapshot of a company's financial position at a specific point in time. They help stakeholders make informed decisions. There are three main types of financial statements: the income statement, the balance sheet, and the cash flow statement. Each plays a crucial role in painting a full picture of the financial standing of a business.

The Income Statement

Think of the income statement as a report card for a company's profitability over a certain period. It details the revenue, expenses, and profits or losses. The goal is to determine the net income, which is the profit after all expenses are deducted from the total revenue.

Here's a basic structure of an income statement:

Revenue

- Cost of Goods Sold

= Gross Profit

- Operating Expenses (like salaries, rent, utilities)

= Operating Income

- Other Expenses (like taxes, interest)

= Net Income

For instance, if a company made $200,000 in sales, spent $80,000 on goods, and had $50,000 in operating expenses, its net income would be calculated by subtracting these expenses from the revenue.

The Balance Sheet

The balance sheet is like a photograph of a company's financial position at a single point in time. It includes assets, liabilities, and shareholders' equity, and it follows this simple formula:

Assets = Liabilities + Shareholders' Equity

Assets are everything the company owns. Liabilities are what it owes. Shareholders' equity is the net worth of the company. Let‘s break these down:

- Assets: This can be cash, inventory, property, equipment, etc.

- Liabilities: These are debts or obligations, such as loans or accounts payable.

- Shareholders' Equity: This is the residual interest in the assets of the company after deducting liabilities.

For example, if a company has assets worth $500,000 and liabilities of $300,000, the shareholders' equity would be $200,000.

The Cash Flow Statement

The cash flow statement shows how cash moves in and out of the business over a period. It is divided into three sections: operating activities, investing activities, and financing activities. Here‘s a quick breakdown:

- Operating Activities: Day-to-day business transactions that affect cash flow, such as receipts from sales of goods and payments to suppliers.

- Investing Activities: Transactions involving the purchase or sale of long-term assets, like property or equipment.

- Financing Activities: Transactions that alter the equity and borrowings of the business, such as issuing shares or repaying bank loans.

For example, if a company receives $150,000 from operating activities, spends $50,000 on new equipment, and pays out $20,000 in loan repayments, the net cash flow would be $80,000.

Gathering the Necessary Information

Before you can create a financial statement, you need to gather all relevant financial data. This includes sales records, purchase records, payroll information, tax documents, and previous financial statements if available. Having everything at your fingertips will make the process much smoother.

Organizing Your Financial Data

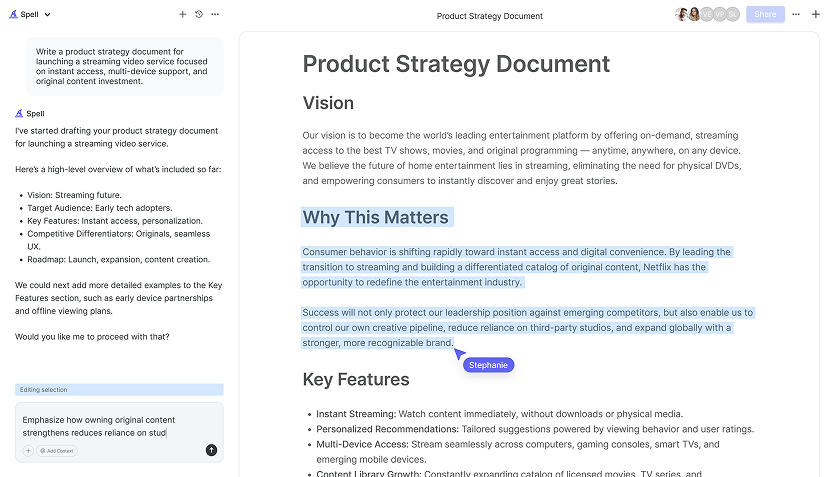

Once you have all the necessary information, the next step is to organize it. Sort your data into categories that align with the sections of the financial statement you're preparing. Use spreadsheets to keep everything orderly. Software like Spell can help streamline this process by allowing you to organize and edit documents efficiently with AI support.

Creating the Income Statement

Let‘s start by putting together an income statement. Begin by listing all revenue sources for the period you‘re assessing. Then, list all expenses, categorizing them into COGS and operating expenses. Subtract the total expenses from the total revenue to find your net income.

Here's a mini example to illustrate:

Revenue: $150,000

- COGS: $60,000

= Gross Profit: $90,000

- Operating Expenses: $30,000

= Operating Income: $60,000

- Other Expenses: $10,000

= Net Income: $50,000

This example shows a simplified income statement where a company ends up with a net income of $50,000 after accounting for all costs and expenses.

Building the Balance Sheet

Next up is the balance sheet. Start by listing all assets, such as cash, inventory, and property, and then do the same for liabilities, like loans and accounts payable. Calculate the shareholders' equity by subtracting total liabilities from total assets.

Let's see an example:

Assets:

Cash: $100,000

Inventory: $50,000

Property: $150,000

Total Assets: $300,000

Liabilities:

Loans: $120,000

Accounts Payable: $30,000

Total Liabilities: $150,000

Shareholders' Equity: $150,000

In this example, the company's assets and liabilities balance out, with shareholders' equity calculated as $150,000.

Drafting the Cash Flow Statement

Now, let's tackle the cash flow statement. Start by documenting cash inflows and outflows for operating activities, followed by investing and financing activities. The net change in cash flow is the sum of these three sections.

Here's a simple example:

Operating Activities:

Cash from Sales: $100,000

Payments to Suppliers: $40,000

Net Cash from Operating: $60,000

Investing Activities:

Purchase of Equipment: $20,000

Net Cash from Investing: -$20,000

Financing Activities:

Loan Repayment: $10,000

Net Cash from Financing: -$10,000

Net Change in Cash: $30,000

In this scenario, the company has a positive cash flow of $30,000 after accounting for all activities.

Reviewing and Adjusting Your Statements

With your financial statements drafted, the next step is to review and adjust them. Look for any inconsistencies or errors. Make sure everything aligns with your financial records. Double-check the math. Even small errors can lead to significant discrepancies.

Using Tools for Accuracy

To enhance accuracy, consider using tools like Spell. It assists in refining documents with AI, ensuring your financial statements are polished and error-free. Plus, it helps with collaboration if you're working with a team.

Finalizing and Presenting Your Financial Statements

Once you're satisfied with the accuracy and presentation of your financial statements, it's time to finalize them. Make sure they're well-organized and easy to read. If you're presenting them to stakeholders, consider adding notes to explain specific figures or decisions.

Common Mistakes to Avoid

While creating financial statements, it's easy to make mistakes. Here are some common pitfalls to watch out for:

- Overlooking expenses: It's essential to account for all expenses, no matter how minor they may seem.

- Mixing personal and business finances: Keep these separate to ensure clarity and accuracy.

- Ignoring cash flow: Even if a business is profitable on paper, poor cash flow management can lead to problems.

Avoiding these mistakes can save you time and headaches down the line.

Using Software to Streamline the Process

Creating financial statements manually can be time-consuming. That's where software comes in handy. Tools like Spell can automate parts of the process, allowing you to generate drafts quickly and refine them with ease. This not only saves time but also reduces the risk of human error.

Continuous Learning and Improvement

Financial statement preparation is a skill that improves with practice. Stay updated with accounting standards and practices, and don't hesitate to seek feedback. Over time, your proficiency will increase, making the task much more manageable.

Final Thoughts

Crafting financial statements doesn't have to be overwhelming. By understanding each type of statement and taking a step-by-step approach, you can create clear and accurate documents. Tools like Spell can make this task even easier, offering you a faster way to draft and refine your statements. Happy accounting